It’s groundhog day for financial services.

More than a decade after the great financial crash of 2008, the tools and methods of financial services remain dangerously unreformed, while experiments in social responsibility have apparently come to naught.

Those who take the reins of the financial services industry – regulators, central bank governors, financial professionals – increasingly recognise that they must meet these challenges with an open mind, not seek to preserve the status quo. The issue is not merely one of the reputation of finance but in fact the purpose of financial services: what they are for and whether they serve the needs of society.

Clearly those needs are not being served by the current arrangements. Environmental degradation, rampant inequalities – especially of place – asset price inflation and concentration have been exacerbated by our system of finance.

The current financial services sector’s productivity has remained static and, by some estimates, has reduced over the last 40 years. Seriously.

Financial regulators and governors recognise that they must serve the whole of society – not just financial markets who remain content to continue as usual, so long as their principals make money. But how?

Financial system change (is hard to do…)

Anyone who has been following this agenda for a while knows that countless programmes and initiatives have emerged that seek to turn this ship around. They are often couched in terms of ‘restoring trust’ in financial services, the business community, or even the wider system of capitalism. Several of them are backed by incredible networks and sums of money. The OECD is bringing European-wide networks together in service of this aim. The UK’s fantastic Finance Innovation Lab encourages new, pro-social financial innovation. Countless private foundations and international think tanks have their own financial reform research programmes.

We are pleased to note that, within different parts of the financial services system, RSA Fellows are leading the charge. David Pitt-Watson FRSA and Dr Hari Mann’s work on bringing purpose to financial services education brings the real prospect of public ethos to our often all-too-insular business schools. Andy Agathangelou FRSA, through his Transparency Task Force initiative, brings practitioners together from all over the world to foreground transparency and financial reform in practice.

Alongside these initiatives are broader movements that seek to bring financial services within the ambit of civil society. Consider employee ownership, shareholder activism, CSR, shared value, triple bottom line and many more besides. Consider the divest-invest movement: the RSA recently divested of any companies that have more than a tithe invested in fossil fuels.

Then there are the frontiers. How do we use venture capital industry intrapreneurship to take silicon-valley investment away from long term social value destruction? How do we support or improve the restorative investment movement? This would mean making up for historical ‘unethical’ investments with investments that directly resolve those problems: divesting from oil and investing consciously and restoratively in green tech might be one example.

The point is that these movements all have merit at some level, but none of thealone have proven to have any sort of system-wide or system-shifting impact. Indeed, the outputs of the financial services sector are so diverse and the inputs so diffuse that the idea of a system change might seem a pipedream from the start

But is it?

The RSA approach to system change

Throughout 2019 the RSA Economy team has been engaging in design thinking in order to reframe and create solutions around apparently intractable economic challenges.

The RSA's Future Work Centre has used design thinking to bring employers and employees together to resolve labour market challenges from automation. The RSA’s Tech and Society Programme has designed deliberative processes to understand how artificial intelligence will change our businesses and public services.

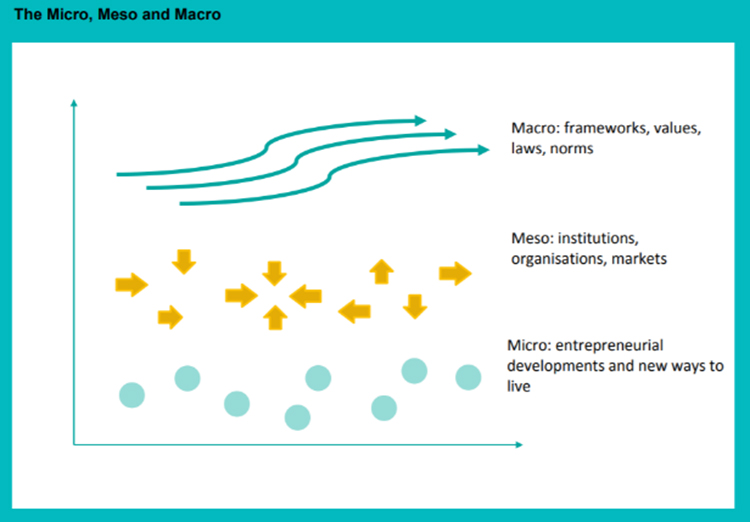

Design thinking is a powerful tool; it allows us to reconceptualise systemic challenges and extract them from big-picture, thematic and ground-level concerns. At the RSA we refer to this as the ‘meso’ level, that sits between ‘macro’ and ‘micro’ level interventions.

On a human level, we are so used to professors, business people and workers alike sticking to their prejudices. With design thinking you take usual frames of reference – like a roundtable – and deconstruct them at that meso level. The ultimate effect of these game-like processes is to say ‘the contribution you usually give is not sufficient, not if we wish to collaborate on real system-level reform.’ And so people of experience are compelled to move into different frames, give a new level of insight – and open themselves up to new levels of ideas sharing through interactivity and play. It all sounds a bit new-age, we know, but don’t take our word for it. The RSA has been involved in a long running BBC radio series showcasing these methods called ‘The Fix,’ presented by our colleagues Matthew Taylor and Rebecca Ford.

Design thinking has been used to think about financial services reform before. The FCA’s Project Innovate, aimed at supporting businesses develop products and services to improve customer experience as well as increasing competition, added a sandbox unit in 2015. Taking participants through a process of iterative design, the sandbox has enabled early stage start-ups, challengers and incumbent firms to test innovative propositions in the market with real consumers.

With the banking sector going through a period of significant disruption, design thinking may well be used more frequently by both challenger banks and existing players to gain competitive advantage. We can see this from Capital One Labs which helped change the way customers and the industry think about banking and moreore recently in new products such as Quickbiz Loans in Autralian and the Bank of America’s Keep the Change Savings product. It’s clear these methods will be at the heart of designing products and services in to the 2020s.

At the RSA our focus is less on devising or scaling individual innovations at the micro level (interesting for VC firms though that is) and less in creating macro level intellectual frameworks for change (interesting for boffins though that is). It’s on the intermediate, system level – the meso level – where groups of actors collaborate through design methods to reform the system.

Here’s our hypothesis: design at the meso level is the missing link. It can help to bring innovations and movements together to create a radical yet practical vision for the financial system’s future.

From method to content

What do we want our financial services industry to do for us? How do we take the global industry from where it is now to where we need it to be? How do we bring reform movements together? This is the discussion the Economy team is starting through the RSA’s emerging Radical Finance Hub.

Purpose must be the first port of call on this journey: what we want the system to do?

Perhaps the story here is around assets. The UK economy is increasingly unbalanced and skewed towards asset price inflation. Banks pour money into bidding up the value of pre-existing assets, with only £1 in every £10 they lend supporting non-financial firms. Introducing measures to guide credit and venture capital investment away from speculation and towards more productive activities is crucial.

Or we face economic insecurity. Financial bubbles and shocks affect the poorest most in the absence of economic resilience. Financial services were originally designed to allow money to be transferred and stored; to promote economy security. Now they engender the opposite effect. Enabling asset-building for all – through savings, pensions, through building businesses and through developing skills – should be a prime purpose of the financial services industry.

What about inequality? With so many businesses and banks moving out of our most deprived areas, the need for a debate around capital concentration and flight on the ground – and how financial services can stem the tide – has never been more acute.

And consider environmental renewal. Financial services – especially venture capital and private equity – should seek to accelerate the transition away from risky fossil fuels and take an active role in positive investment in transition economy ventures. The potential for ethical and responsible investment and ownership is there, in the ether, but yet to be tapped.

And if we want to deliver on all of these purposes or more: can design thinking at the meso level be the missing link?

Designing a new banking system

Let’s remind ourselves that this sort of system-level change in financial services is eminently possible. In fact, at the RSA we’re doing it right now.

Over the course of 2017-19, the RSA has been supporting the Community Savings Banking Association (CSBA) in creating a brand new network of regional banks. These are not banks in theory or on paper, but actual organisations with boards and branches that will take deposits and provide loans and mortgages, once approved by the FCA.

Across the UK this project is at different stages. From South West Mutual, who recently completed their first round of investment and have started the process of applying for their banking licence, to North West, where the political appetite is clearly there but the banks themselves are yet to be established – 2019/20 is set to be an exciting time for this movement.

Designing this layer of banks and this new artefact of the financial services system has involved financiers, politicos, analysts, RSA researchers, Fellows, networks and design expertise.

Moreover, the network has been designed to cover multiple purposes. These banks will support SMEs and the productive economy. They will provide banking where high street banks have vacated the space in search of more traditionally bankable customers. They will act as community hubs to build local economies. They will support green initiatives. They are a layer of infrastructure on which future radical finance reforms can be built, designed and constructed through months of collaboration: an experiment that might succeed or fail on its own terms but at any rate gives us insight into just what is possible when design and reform coincide.

Is it really utopian or reductive to think that community banking is just the start?

Next steps

We think that the RSA is at the beginning, not the end of this journey. Knowhow, design thinking, expertise, influence, teamwork, global reach, Fellowship networks: these are the RSA assets we seek to bring together to create a real step change in the financial services system, from how Silicon Valley VCs invest to how global and local generational banking products are designed and distributed, to education, policy framing and more besides.

From building new prototypes and products to effect system-level change, to scenario planning (as the RSA did in the Future Work Centre) and gaming the financial industry’s future to 2050, to seeking new ways to bring radical financial products to local communities, to shifting the financial education and self-assessment architecture, our ambition is unapologetically wide.

And now comes the ask. We can’t change systems without RSA Fellows and the wider thought and practice community; without thinkers, activists, investors, fund managers, and others. The question from us is: how do we take this conversation forward?

If you are interested in this work, in getting involved, lending your expertise, staying in touch, joining a collaborative zoom call, or recommending a friend please register your interest with Radical Finance Hub below. We will be running a series of starter events over the course of autumn 2019 and would be delighted to bring you into the conversation.

This article was co-authored by Asheem Singh, Director of Economy and Mark Hall, Deputy Head of Engagement at the RSA. If you have any questions about our work in this area or the emerging Radical Finance Hub, please email Mark at [email protected]

Related articles

-

Can cash survive coronavirus?

Mark Hall

Getting your hands on money has never been so important, yet nobody wants to touch it. Mark Hall explores the urgent need for a more inclusive digital economy.

-

Can we keep cash alive?

Mark Hall

On our current trajectory, we risk sleepwalking into a cashless economy that excludes and divides. As the digital economy expands, can we keep our cash economy alive?

-

Four ways the RSA is supporting the community banking movement to make an impact

Mark Hall

Mark Hall outlines four key ways in which we are supporting the community banking movement to make an impact.

Join the discussion

Comments

Please login to post a comment or reply

Don't have an account? Click here to register.

At last! This sounds like the initiative I have been hoping the RSA would take since I became a Fellow. I've written on several of the themes mentioned here, including the need for more productive non-financial investment and promoting greater financial stability. For me the ultimate purpose of the industry is to help bring about the future society that a) we want to achieve and b) we expect to see. Among other things that means allowing for far greater financial adaptability and flexibility in peoples' lives (something else I have written on) and helping to ensure the world of the future is one we want, and are able, to live in. When finance enables better lives for all it won't need to worry about its social licence to operate. Asheem: I'll drop you a separate email - I hope that's OK