Mark Hall introduces new research from the RSA on Britain’s relationship with cash and digital payments that shows 10 million people would struggle in a cashless society.

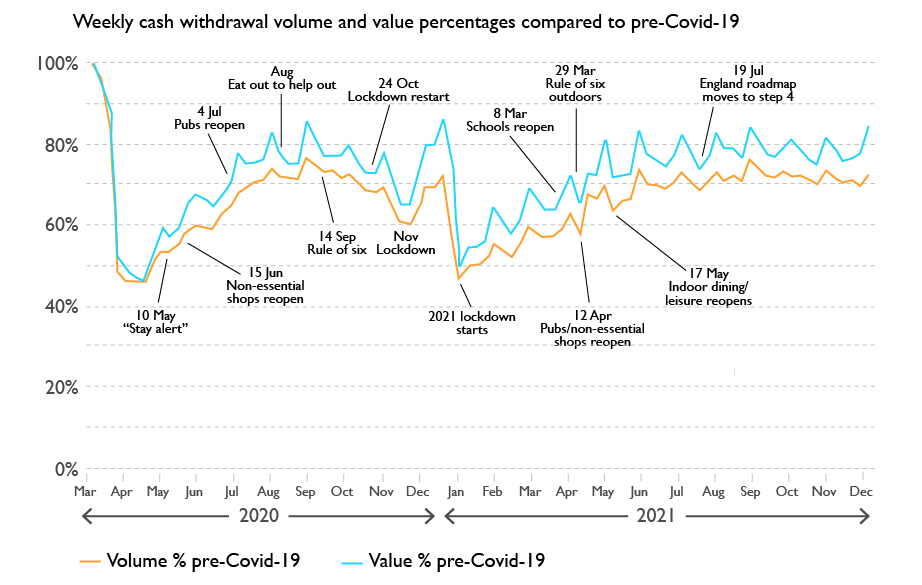

The decline of cash is not a new phenomenon. The last decade has seen a rapid rise of digital banking and payments and the Covid-19 pandemic has only accelerated digital payments at a pace even industry professionals could not have predicted.

The cash census

Explore the use of cash in an increasingly digital economy.

Millions benefit from fintech innovations that make their lives more convenient. And yet, at the same time, many feel forced into a world for which they are ill-equipped.

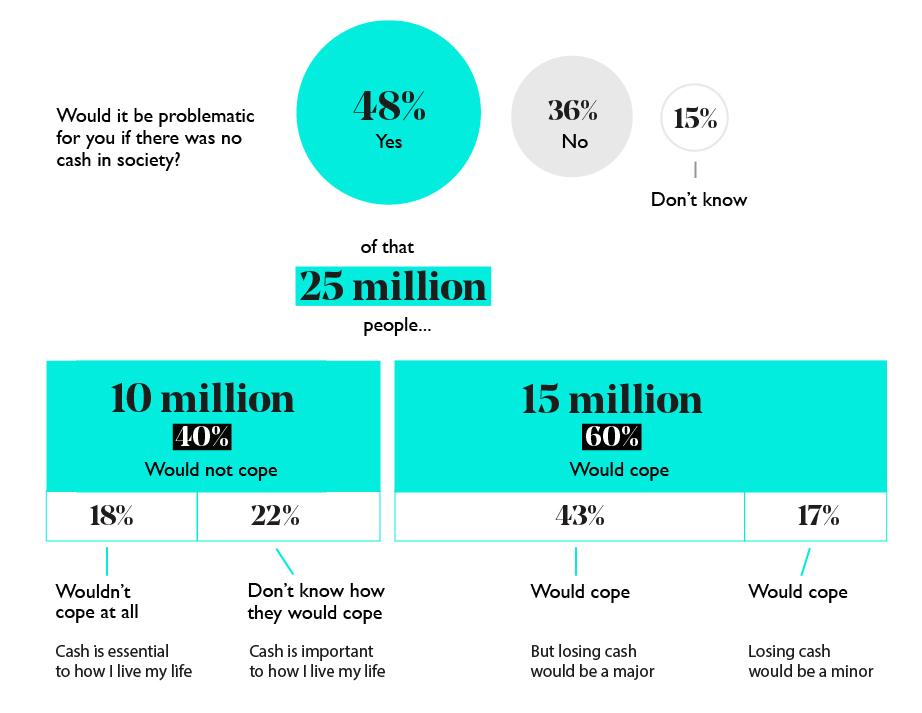

The Access to Cash Review, led by Natalie Ceeney CBE in 2019, highlighted that around one in five people would struggle to cope in a cashless society. The RSA’s latest report, The cash census – an in-depth study into Britain’s attitudes and behaviours around cash and digital payments - show that despite the pandemic turbocharging the transition to more digital payments for many, 10 million people would still struggle to cope in a cashless society. For millions more, it would be a major inconvenience.

This blog will introduce the five segments of the UK population and their differing attitudes and relationships with cash and digital payments.

This blog will introduce the five segments of the UK population and their differing attitudes and relationships with cash and digital payments.

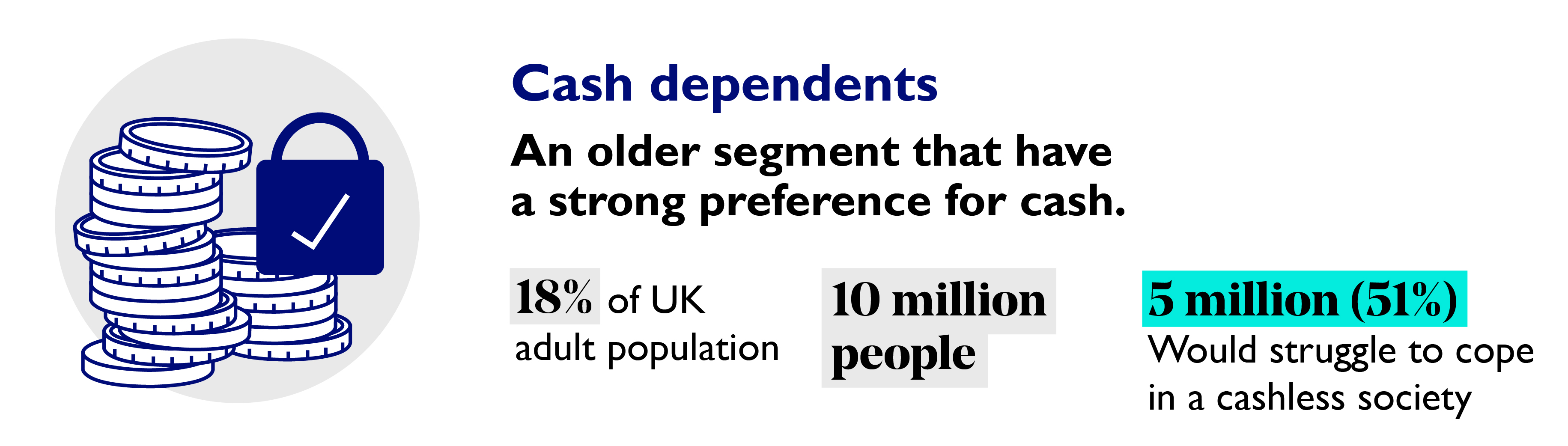

Cash dependents

Cash dependents rely on cash for budgeting and tend to make regular withdrawals. This segment has the highest dependence on cash as it makes those within it feel in control of their finances. They are the segment that would struggle the most switching to digital payments and living in a cashless society.

Cash dependent John is in his early sixties and lives in North West England. He uses cash regularly as it helps him manage his spending and it makes him feel in control of his finances.

It may be an age thing, but I prefer to control my finances by having cash.

He likes to keep a familiar routine to ensure he always has cash to budget for the month ahead. John’s bills are all set up to go out within a few days of him being paid. This enables him to know exactly what he’s got left for the month ahead. He has previously got into debt using credit cards as he lost track of his spending. He feels strongly that the digitalisation of the economy is forcing a generation towards ‘a challenge they are not ready for’.

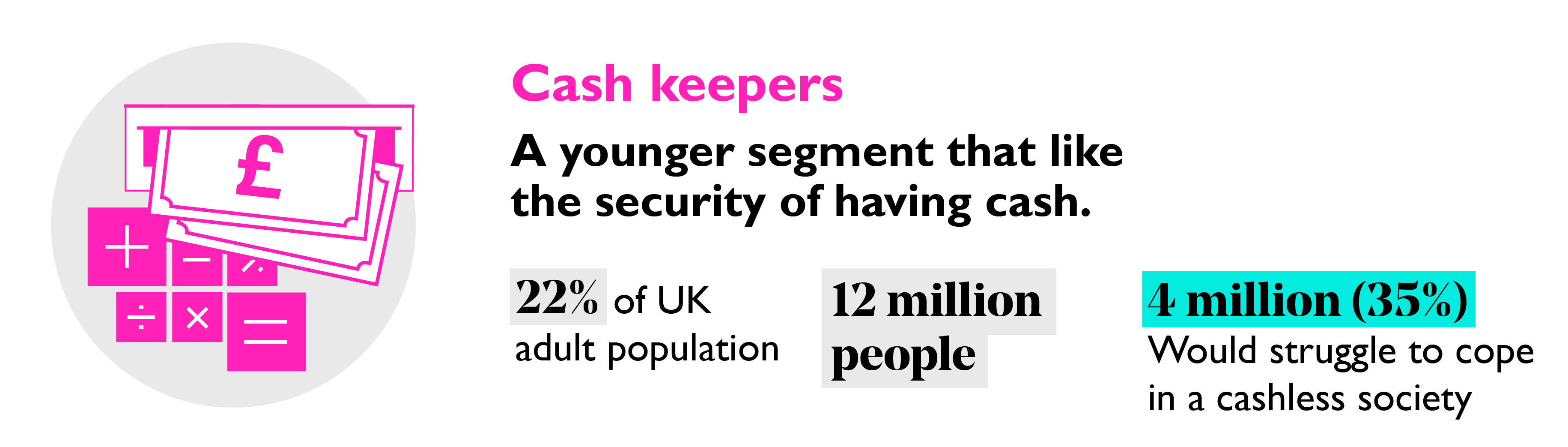

Cash keepers

The youngest segment, with the majority living in urban areas. Cash keepers tend to make relatively frequent withdrawals and are the most likely segment to keep cash at home. While most are using digital payment methods, around a third have difficulties accessing digital payments and a similar number don’t trust card payments. The majority find it easier to track spending using cash which makes them feel more in control of their finances.

Cash keeper Anita is in her mid-30s, she lives in East London with her two children. She uses digital payments but was initially reluctant to use contactless payments when they were introduced as she wasn’t sure if it was secure or if she might be charged twice.

While she predominantly uses digital payments, she does like to keep cash at home and uses cash to budget for things, particularly at the end of the month. She likes that you can only use the cash you have and can’t keep spending money you don’t have.

She has also had personal experience of fraud when using digital payments and previously had problems remembering her PIN, so she likes to have cash on her as a backup.

“I was using PayPal and I used to get this email all the time asking me to update my account details. At that time, I was new to it, and I added all the details and I got defrauded… Now I think twice about having my details stored online.”

A cashless society would present some challenges for Anita. Her main concerns would be around fraud and the problems this would cause for small businesses.

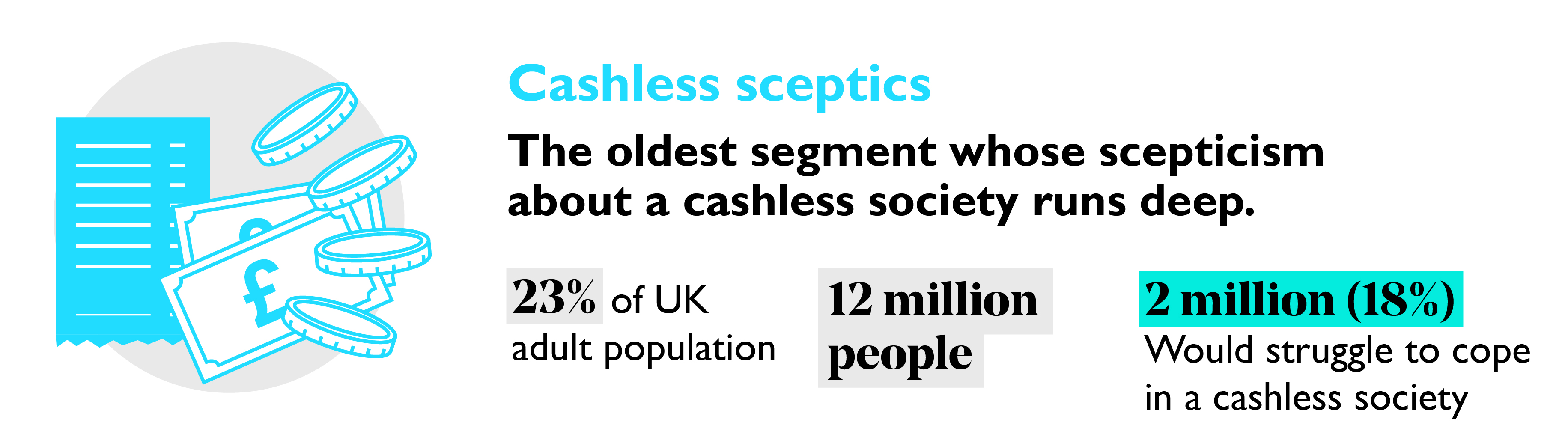

Cashless sceptics

The oldest segment with the majority living in rural or suburban areas. They are generally in control of their finances and have strong concerns about fraud with digital payments. Losing cash would be inconvenient for around half but the majority would cope. They have a strong attachment to cash and are very sceptical about the idea of a cashless society.

Cashless sceptic Anne is in her early 50s and she lives a short drive outside Leeds in West Yorkshire. She’s happy using contactless payments for most purchases but doesn’t like to rely on it as she can often have poor phone signal. She also finds cash easier for splitting bills, paying local tradesmen, treating grandchildren, and tracking spending. Anne keeps track of all her payments using a spreadsheet, whether they are digital or cash transactions.

For Anne, cash performs a really important ‘social function’.

“At Christmas, I like to give the postman a fiver just to have a drink and the dustbin men and people like that, just a little gesture. And I think, you know, you can just be more human … you can’t just say give me your PayPal address!”

Anne also has some real concerns about fraud and privacy when using digital payments.

“I do worry about fraud or having my card/phone stolen and it being too easy for people to use due to the contactless facility.”

Anne would be able to cope in a cashless society, but it wouldn’t be her preference.

Cash occasionals

A younger tech-savvy segment that tends to prefer the convenience of digital payments. The cash occasionals are open to a cashless society but many have strong concerns about fraud and privacy in digital payments and view cash as useful in emergencies or for small purchases.

Andrea is in her late 20s and lives on her own in a flat 20 minutes outside of Newcastle. She has a debit card with a high street bank which she uses for almost everything. She also has a card with an online-only bank which she uses for travelling overseas as it avoids the conversion fee. Andrea much prefers to use digital payments and although she doesn’t use other forms of digital payment at the moment, she is considering using mobile payments in the future.

“Digital is good for purchasing internationally. It opens up the world to possibilities. If I buy something from France or Germany they’re not going to wait for the cash and won’t want it in pounds.”

Andrea tends to keep a small amount of cash on her in case of emergencies and only visits the cash machine every couple of months to top this up when needed.

“Generally, I keep between £5 and £10 on me to use in a shop if they don’t accept card or to cover something urgent, like when my phone dies and I can’t access my bus ticket [QR code], then I need to pay in cash.”

Andrea feels confident using the internet and feels able to spot scams. She’s never been a victim of fraud.

“If I had [been a victim of fraud] I might be more wary warier… I’d be more concerned losing £50 in cash than losing my debit card as I can quickly cancel it and the bank will refund me.”

While Andrea is very happy about the increasing use of digital payments, she would be slightly wary about a cashless society.

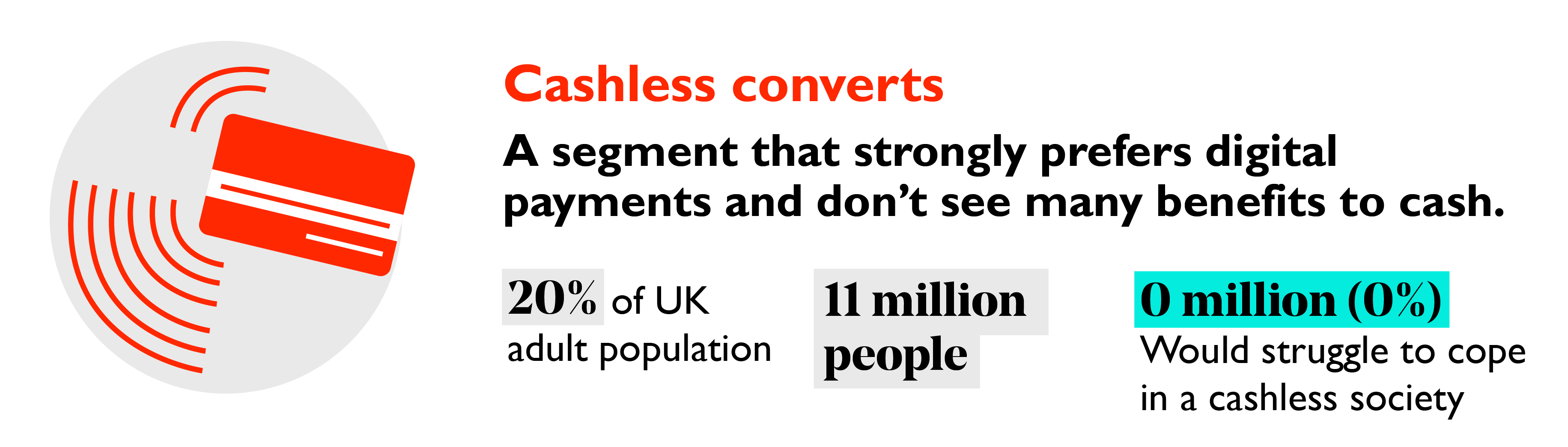

Cashless converts

Well represented across all age groups, the cashless converts are in control of their finances and see few benefits to cash, other than in emergencies. This segment is the most comfortable with technology and hardly uses cash at all. A cashless society would feel like progress for the majority, and all could cope with such a transition.

Cashless convert Andrew is in his early 40s, he works in the finance industry and lives with his family just outside Sheffield. He predominantly uses a card or Apple Pay and can’t recall the last time he used cash. Andrew has several debit and credit cards with different banks and uses online and mobile banking to manage his finances. Open banking has allowed him to easily manage his accounts across a range of digital platforms. He only uses cash when he has no alternative option.

He is less concerned about fraud with digital payments.

“I'm pretty happy [with payment technology]. When you buy something online, you can make sure it's got a lock icon [and] that it's a secure website, make sure you don't give your card details to somebody who rings you up, or sends you an unsolicited email, that sort of thing. [A cashless society] would not impact me much, society would adapt, and about 99.99 percent of my purchases are done via card and apple pay.”

A sudden shift to a cashless society would be a major challenge for millions of cash dependents and cash keepers without the capabilities to engage in the economy. It would limit the agency and control many have over managing their finances. While the more financially secure cashless sceptics, cash remains an essential tool to connect with their community.

We propose a series of recommendations for policymakers, regulators and across industry to support those who still rely on cash to access it when they need it and support everyone’s transition to a more digital economy – find out more in The cash census report.

To learn about the breakdown of behaviours and attitudes towards cash by area of the country, explore our regional dashboard.

What are your experiences using cash today? Why do you choose the make payments the way you do? Do you have a view on the direction we are going with it comes to our relationship with cash. Let us know in the comments below.

Related articles

-

The cash census

Report

Mark Hall Asheem Singh James Morrison Aoife O'Doherty

This new piece of RSA research explores the use of cash in an increasingly digital economy.

-

Card or cash? Patterns of cash-use in the UK

Blog

James Morrison

Researcher James Morrison looks at the relationship between cash use and deprivation.

-

Is Britain ready to go cashless?

Research & Impact Event

Online

As digital payments and banking boom, is Britain ready to go cashless? Join our webinar to discuss the future of cash.

Join the discussion

Comments

Please login to post a comment or reply

Don't have an account? Click here to register.

Excellent report - very interesting picture you paint and some great recommendations. I hope the government and regulators are listening and respond.